With all the excitement last week surrounding the SEC’s release of the final Title III rules implementing “Regulation Crowdfunding,” the SEC’s vote in favor of proposing amendments to the current Rule 147 to help foster Intrastate Crowdfunding amounted to little more than a side-note. Given my own personal interest in the world of Intrastate crowdfunding however, I was quick to dive into the proposed amendments. While, on the whole, the SEC made some very solid proposals to help modernize the outdated rule, there was one proposed amendment to Rule 147 that, if successful, would essentially make all of the other proposed amendments to Rule 147 completely moot for Issuers in most states.

With all the excitement last week surrounding the SEC’s release of the final Title III rules implementing “Regulation Crowdfunding,” the SEC’s vote in favor of proposing amendments to the current Rule 147 to help foster Intrastate Crowdfunding amounted to little more than a side-note. Given my own personal interest in the world of Intrastate crowdfunding however, I was quick to dive into the proposed amendments. While, on the whole, the SEC made some very solid proposals to help modernize the outdated rule, there was one proposed amendment to Rule 147 that, if successful, would essentially make all of the other proposed amendments to Rule 147 completely moot for Issuers in most states.

The Proposed Amendments:

The stated purpose of the SEC’s proposed amendments to Rule 147 is to modernize the archaic rule in order to align it with contemporary business practices; in particular, the unavoidable use of the Internet. For those that don’t know, Rule 147 is the basis for “intrastate crowdfunding.” Technically, Rule 147 currently exists as a “safe harbor” under Section 3(a)(11) of the Securities Act of 1933 (the “Act”) which provides an exemption from registration (emphasis added) for “any security which is a part of an issue offered and sold only to persons resident within a single state or territory, where the issuer of such security is a person residing and doing business within, or, if a corporation, incorporated by and doing business within such state or territory.” This is really a long winded way of saying that a securities offering that taxes place completely within one state is exempt from federal registration.

long winded way of saying that a securities offering that taxes place completely within one state is exempt from federal registration.

The problem with Rule 147 is that is has not substantively changed since it was adopted in 1974 so it is horribly out of date with today’s internet dependent world. The SEC’s proposed amendments to Rule 147 include three major changes to the existing Rule: 1) eliminating the restriction on “offers” being made only within a state (while still continuing to require that sales be made only to residents within the state); 2) eliminating the requirement that an Issuer actually be “incorporated” (or formed, organized, etc.) within the state where the offering is taking place; and 3) redefining what constitutes “doing business” within a state. In addition to these main changes, the SEC is also proposing amendments to help simplify/clarify the integration rules, the verification of investor residency status, and the resale and holding period restrictions, with respect to Rule 147 offerings.

1) Elimination of Limitation on Manner of Offering

The problem with the existing Rule 147 is that it does not permit Issuers to use any form of general solicitation/advertising to promote their offering which could potentially reach, or be seen by, out-of-state residents. Instead an Issuer can only engage in solicitation/advertising which is narrowly targeted to in-state residents only. As I am sure you can imagine, this makes the use of the internet (including social media) virtually impossible. While the SEC has issued some guidance over the past year which permits limited use of the internet to advertise Rule 147 offerings, using the internet to promote such offerings while still remaining compliant with Rule 147 remains extremely tricky.

limited use of the internet to advertise Rule 147 offerings, using the internet to promote such offerings while still remaining compliant with Rule 147 remains extremely tricky.

The proposed amended Rule 147 would focus only on where the actual sale of securities occurred and would ignore how, and by what means, an offer was made. Put another way, the proposed amended Rule 147 continues to limit sales only to in-state residents but “would no longer limit offers by the issuer to in-state residents.” As noted in the SEC’s proposal, under the amended Rule 147, Issuers would be permitted to “engage in general solicitation and general advertising that could reach out-of-state residents in order to locate potential in-state investors using any form of mass media, including unrestricted, publicly available websites, to advertise their offerings.”

The permitted use of general solicitation is a huge leap forward in modernizing Rule 147. The only caveat to the use of such general solicitation is that, under the proposed amendments, all offering materials will need to include a “prominent disclosure” stating that sales will be made only to residents of the Issuer’s state. A small price to pay for being able to advertise an offering over the internet without fear of violating Rule 147.

2) Elimination of Residence Requirement for Issuers.

The current Rule 147 requires Issuers to be incorporated/organized/formed in the state in which the intrastate offering is conducted. As noted by the SEC “[t]his requirement, while based on the language of Section 3(a)(11), is at odds with modern business practice in which issuers incorporate or organize in states other than the state or territory of their principal place of business, for example, to take advantage of well-established bodies of corporate or partnership law.” The SEC’s proposed amendments would eliminate the current “residence” requirement and replace it with a “principal place of business” standard (NOTE: The same standard would apply for general partnerships and other forms of business organizations not organized under state law).

standard (NOTE: The same standard would apply for general partnerships and other forms of business organizations not organized under state law).

Under the proposed amendments, an Issuer would be permitted to conduct a Rule 147 offering in the state in which its “principal place of business” is located, regardless of where the Issuer is actually incorporated/ organized/ formed. As proposed, an Issuer’s “principal place of business” would be the “location from which the officers, partners, or managers of the issuer primarily direct, control and coordinate the activities of the issuer.” While this definition could clearly be read to include more than one state, under the proposed rules an Issuer would only be able to have a “principal place of business” within a single state and would therefore only be able to conduct a Rule 147 offering within that state. Further, under the proposed rules, should an Issuer who conducts a Rule 147 offering in one state subsequently move their operations to another state, the Issuer would not be able to conduct a Rule 147 offering in the new state for a period of nine months from the closing of last Rule 147 offering.

3) Requirements for Issuers “Doing Business” In-State.

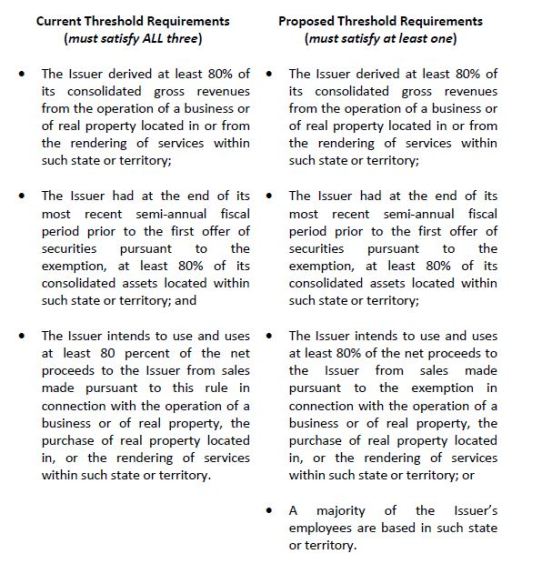

In addition to the requirement that an Issuer be incorporated/ organized/ formed in the state in which the offering occurs, the current iteration of Rule 147 includes three threshold requirements (shown below), each of which an Issuer must satisfy in order to be

considered “doing business” in the offering state. These threshold requirements were intended to adhere to the concepts of Section 3(a)(11) and ensure that, not only would the Issuer be physically located within the offering state, but also that the Issuer’s predominant business is carried on, and substantially all of the proceeds of the offering would be put to use, within such state. In today’s internet based society, meeting any one of these thresholds can be extremely difficult, let alone all three.

the Issuer be physically located within the offering state, but also that the Issuer’s predominant business is carried on, and substantially all of the proceeds of the offering would be put to use, within such state. In today’s internet based society, meeting any one of these thresholds can be extremely difficult, let alone all three.

The proposed amended Rule 147 still includes the same three threshold requirements as under the current rule. However, it also includes a fourth, more general, threshold requirement, and would only require that an Issuer satisfy one, not all, of the stated threshold requirements. Both of these changes would make compliance with Rule 147 significantly easier for Issuers.

4) Additional Amendments.

As noted above, the proposed amendments to Rule 147 also include positive changes related to the rules governing the integration of Rule 147 offerings, the verification of investor residency status, and the resale and holding period restrictions. These proposed changes are as follows:

- Integration. Under the current rule, an offering made under Rule 147 would not be integrated with offerings made more than six months before, or six months after, any Rule 147 offering. The proposed rules simplify and expand the current integration rules by providing that an offering made under Rule 147 would not be integrated with: prior offers or sales of securities (regardless of when the offering occurred); or subsequent offers or sales of securities that are:

- Registered under the Act (with limited exception);

- Exempt from registration under Regulation A (§ 230.251 et seq.);

- Exempt from registration under Rule 701 (§ 230.701);

- Made pursuant to an employee benefit plan;

- Exempt from registration under Regulation S (§§ 230.901 through 230.905);

- Exempt from registration under section 4(a)(6) of the Act (15 U.S.C. 77d(a)(6)); or

- Made more than six months after the completion of an offering conducted under Rule 147.

- Verification of Investor Residency Status. Under the current Rule 147, and regardless of the efforts taken to determine whether an investor is an in-state resident, the exemption would be lost for the entire offering if securities are offered or sold to an investor who was not, in fact, a resident of the state. The proposed amendments would eliminate this draconian result by providing for a “reasonable belief” standard (consistent with the requirements in Regulation D) in determining the residence of a purchaser at the time of the sale of the securities. As proposed, an Issuer would be able to satisfy the requirement that securities be sold to in-state residents by establishing that the Issuer had a “reasonable belief” that the purchaser of the securities in the offering was a resident at the time of sale.

- Resale and Holding Period Restrictions. Under current Rule 147(e), “during the period in which securities that are part of an issue are being offered and sold by the issuer, and for a period of nine months from the date of the last sale by the issuer of such securities, all resales of any part of the issue, by any person, shall be made only to persons resident within such state or territory.” As a result, the holding period for one purchaser could be significantly longer than for another purchaser. For example, a purchaser who invested at the beginning of an offering would need to hold the securities until the offering was completed and for an additional period of nine months. On the other hand, a purchaser who invested at the end of an offering would only need to hold the securities for nine months. The proposed amendments seek to simplify the holding period rules by simply requiring purchasers to hold the security for nine months, regardless of when the offering is completed.

The Major Problem:

As stated earlier, there is one provision of the proposed amendments that could potentially make all of the beneficial amendments above completely moot for Issuers in most states. That provision at issue is the SEC’s proposal to make Rule 147 function as a separate exemption from registration under the Act rather than as a “safe harbor” under Section  3(a)(11) of the Act. If Rule 147 and Section 3(a)(11) are treated separately, many Issuers would simply not be able to use any of the above provisions. Let me explain.

3(a)(11) of the Act. If Rule 147 and Section 3(a)(11) are treated separately, many Issuers would simply not be able to use any of the above provisions. Let me explain.

First, as noted by the SEC, the proposed amended Rule 147 “would no longer fall within the statutory parameters of Section 3(a)(11).” Second, the proposed amendment specifically “limit[s] the availability of Rule 147, as proposed to be amended, to issuers that … conduct the offering pursuant to an exemption from state law registration in such state that limits the amount of securities an issuer may sell pursuant to such exemption to no more than $5 million in a twelve-month period and that limits the amount of securities an investor can purchase in any such offering.” The only provisions that currently meet these criteria are the existing and proposed state-based crowdfunding statutes. However, since nearly all currently proposed state-based crowdfunding statutes (other than Maine and Mississippi) require compliance with Section 3(a)(11) (which we already established cannot be done under the proposed new rules), Issuers in these states would not be able to utilize the enhanced provisions of amended Rule 147 and still be in compliance with state law. Soooooooo where does that leave us? I am glad you asked. It leaves us with a document filled with beneficial amendments to an outdated rule that no one (other than those Maine and Mississippi) can take advantage of.

The SEC even acknowledged the fact that most state-based crowdfunding statutes require compliance with Section 3(a)(11) but simply dismissed the issue by saying “states that have crowdfunding provisions based on compliance with Section 3(a)(11), or compliance with both Section 3(a)(11) and Rule 147, would need to amend these provisions in order for issuers to take full advantage of these amendments.” An Amendment to the state rules? Sure, why not, it only took most states years to get a crowdfunding law on the books, how hard can it be to get an amendment. Piece of cake SEC, no problem! (sarcasm added)

Not only would an amendment to each of the existing and proposed state-crowdfunding statutes be extremely difficult and time consuming to obtain (if it could even be obtained), it simply is not necessary or warranted. The SEC has provided no definitive reason for wanting to have Rule 147 treated as a separate exemption and, given the clear adverse effect that would result, it should not be treated as such. Moreover, keeping the proposed amended Rule 147 as a “safe harbor” under Section 3(a)(11) is entirely consistent with the existing opinions and guidance issued by legislators and the SEC with respect to Section 3(a)(11).

So, to the SEC, I can only say “stop what you’re doing, cause you’re about to ruin, the image and the style that I’m used to” … (If you don’t know what that quote is from,  you really should). For a more detailed and scholarly version of this statement I refer you to the comment letter I recently submitted to the SEC on this issue. I strongly urge others to address this issue with the SEC in order to prevent them from passing a set of very positive amendments that only Issuers in Maine and Mississippi will be able to use.

you really should). For a more detailed and scholarly version of this statement I refer you to the comment letter I recently submitted to the SEC on this issue. I strongly urge others to address this issue with the SEC in order to prevent them from passing a set of very positive amendments that only Issuers in Maine and Mississippi will be able to use.

I very much appreciate Antony J. Zeoli, and the information as presented here as place we can all get good information well interpreted about crowdfunding issues. Could some one give us a short simplified version of his letter he presents here to the SEC reference rule 147 so we might submit accurately on a layman’s level to the SEC the same sentiment in order to support him and his firm’s ( Feldman) effort on our behalf? Douglas Wilson

Pingback: CFIRA Offers Its Comments To SEC On Proposed Regulatory Changes. | CROWDFUNDINGLEGALHUB.com

Pingback: Massive Amendments To Rule 147 May Be Approved TODAY! | CROWDFUNDINGLEGALHUB.com